In the rapidly evolving landscape of financial technology (Fintech), various services have emerged to revolutionize the traditional financial sector. One prominent category is payment and money transfers and peer-to-peer payment platforms facilitate seamless and efficient transactions.

Another crucial aspect is lending and crowdfunding, where Fintech platforms connect borrowers with lenders, streamlining the loan application process and increasing accessibility to capital. Investment and wealth management have also experienced a significant shift, with robo-advisors offering automated, algorithm-driven financial planning and investment strategies.

Additionally, Insurtech, the intersection of technology and insurance, has introduced innovations such as data analytics and blockchain to enhance risk assessment and policy management. Blockchain and cryptocurrencies represent another dimension, providing decentralized and secure alternatives for transactions and investments.

Lastly, Regtech focuses on regulatory compliance and risk management, utilizing technology to help financial institutions navigate complex regulatory frameworks. Together, these diverse Fintech services exemplify the industry’s transformative impact on the financial landscape, catering to the evolving needs of consumers and businesses alike.

Overview Of the Fintech Industry

Over the last few years, the industry has grown impressively. From 5,868 in 2018 to 11,651 in 2023, there were more financial companies in the Americas alone. But things have really calmed down in the business.

Global fintech funding hit a record $132 billion in 2021, making up 21% of venture capital funding. Fintech company funding fell to $75.2 billion globally in 2022, a 46% decrease from 2021.

Fintech funding has increased by 52% over 2020, so the drop from 2021 to 2022 is probably a correction in the market rather than a sign of a downturn in the sector.

It’s also important to note that, generally, fintech app adoption rates rose by 38% between 2020 and 2022, showing that consumers are still devoted to bettering their financial circumstances and taking charge of their money.

How Does a Fintech Company Work?

A Fintech (financial technology) company operates by leveraging technology to provide innovative solutions for various financial services. The core functions and operations of a Fintech company can be outlined as follows:

Identifying a Problem or Opportunity:

Fintech companies typically begin by identifying inefficiencies, challenges, or gaps in the traditional financial services industry. This could be anything from slow processes and high transaction costs to limited accessibility for certain demographics.

Technology Integration:

Fintech companies utilize advanced technologies such as artificial intelligence, machine learning, blockchain, and data analytics to create solutions that address the identified problems. This could involve developing mobile apps or backend systems to streamline processes and enhance user experience.

Product Development:

After identifying the problem and conceptualizing a solution, Fintech companies develop their products or services. For example, they might create a mobile payment app, a robo-advisor for investment management, or a peer-to-peer lending platform.

User Interface and Experience:

Fintech companies prioritize user-friendly interfaces to ensure that their products are accessible and easy to use for consumers. This often involves designing intuitive apps or platforms that simplify complex financial processes.

Compliance and Regulation:

Given the highly regulated nature of the financial industry, Fintech companies must adhere to relevant legal and regulatory frameworks. This involves ensuring compliance with financial regulations, data protection laws, and other industry-specific requirements.

In summary, a Fintech company operates by leveraging technology to address financial challenges, creating user-friendly solutions, ensuring regulatory compliance, and continually evolving to meet the changing needs of the market.

5 Different Types of Fintech Services

Fintech services encompass a wide range of offerings that leverage technology to enhance and streamline financial processes. Here are five different types of Fintech services:

Payment and Money Transfers:

This category includes digital wallets, mobile payment apps, and peer-to-peer (P2P) payment platforms. Fintech companies in this space facilitate electronic transactions, enabling users to send and receive money seamlessly, make online purchases, and manage their finances digitally.

Lending and Crowdfunding:

Fintech platforms in the lending and crowdfunding sector connect borrowers with lenders, cutting through traditional banking processes. Crowdfunding platforms allow people to raise funds for projects or ventures through small contributions from a large number of individuals.

Robo-Advisory and Investment Management:

These Fintech services use artificial intelligence and data analysis to offer personalized investment strategies, making wealth management more accessible to a broader audience with lower fees compared to traditional financial advisors.

Insurtech (Insurance Technology):

This includes the use of data analytics for risk assessment, artificial intelligence for claims processing, and blockchain for secure and transparent policy management. Insurtech aims to enhance efficiency, reduce costs, and provide more customized insurance solutions.

Blockchain and Cryptocurrencies:

Fintech services related to blockchain and cryptocurrencies involve decentralized and secure alternatives for financial transactions. Cryptocurrencies like Bitcoin and Ethereum enable peer-to-peer transactions without the need for traditional financial intermediaries.

These categories represent just a subset of the diverse Fintech landscape, as the industry continually evolves with technological advancements and changing consumer demands. Other notable areas include Regtech (Regulatory Technology), focusing on compliance and regulatory solutions, and Personal Finance Management apps that help individuals budget, save, and invest.

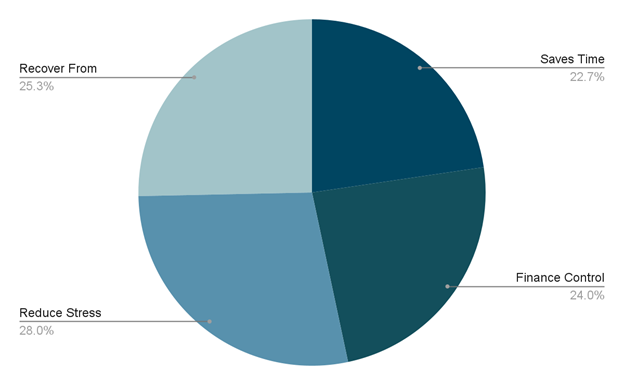

7 Effective Benefits Of Fintech Service

Fintech, or financial technology, has revolutionized the way we manage our money. By leveraging technology, fintech companies offer innovative solutions that provide numerous benefits for both individuals and businesses. Here are 7 of the most effective:

- Convenience and Accessibility: Fintech services are often available 24/7, allowing you to manage your finances anytime, anywhere, from any device. This eliminates the need to visit physical bank branches or wait in long lines.

- Increased Efficiency and Speed: Fintech automates many complex financial tasks, streamlining processes and making transactions faster. Fintech can significantly improve your financial efficiency.

- Personalized Financial Solutions: Unlike traditional banks with standardized offerings, fintech companies use technology to personalize financial products and services based on your individual needs and preferences.

- Greater Financial Inclusion: Fintech can open up access to financial services for underserved communities who may have been excluded from traditional banking systems. Empower individuals and businesses previously left behind.

- Enhanced Security and Fraud Protection: Fintech companies invest heavily in cybersecurity measures to protect your financial data and prevent fraud. Real-time transaction monitoring provides peace of mind and ensures the security of your finances.

- Lower Costs and Fees: By automating processes and reducing reliance on physical infrastructure, fintech companies can often offer lower fees and more competitive rates compared to traditional financial institutions.

- Innovative Financial Products and Services: Fintech is constantly evolving, bringing new and innovative financial products and services to the market. Fintech offers exciting possibilities for managing your finances in new and efficient ways.

Overall, fintech services offer a wide range of benefits that can significantly improve your financial well-being. Fintech is shaping the future of finance and empowering individuals and businesses to take control of their financial lives.

The Most Common Mistakes to Avoid in Industrial Fintech Services

In the rapidly evolving realm of industrial fintech services, companies may encounter various challenges and pitfalls. Here are some common mistakes to avoid:

Neglecting Cybersecurity:

Fintech services deal with sensitive financial data, making them prime targets for cyberattacks. Neglecting robust cybersecurity measures can lead to data breaches, financial losses, and damage to the company’s reputation.

Overlooking Regulatory Compliance:

Fintech services are subject to numerous financial regulations, and non-compliance can result in severe legal consequences. Ignoring or underestimating regulatory requirements can hinder operations and damage trust with clients.

Insufficient Customer Education:

Introducing innovative fintech solutions to industrial clients may require a significant shift in traditional processes. Failing to adequately educate customers about the benefits and proper usage of the technology can lead to resistance and dissatisfaction.

Inadequate Scalability Planning:

Fintech companies must anticipate and plan for scalability from the outset. Rapid growth or changes in demand can strain systems and infrastructure. Insufficient scalability planning may result in downtime, poor performance, and customer dissatisfaction.

Ignoring User Experience (UX) Design:

User experience plays a crucial role in the adoption and success of fintech services. Prioritizing user-friendly design and intuitive navigation is essential to ensure a positive experience and encourage continued engagement with the platform.

Poor Data Management Practices:

Inadequate data management practices, such as poor data quality or insufficient data privacy measures, can compromise the reliability of financial insights and erode customer trust. Implementing robust data governance and compliance measures is vital.

Lack of Interoperability:

In the industrial sector, various systems and technologies may need to interact seamlessly. Failing to ensure interoperability with existing systems can result in integration challenges, data silos, and operational inefficiencies.

Underestimating Change Management:

Implementing industrial fintech services often requires a cultural shift within organizations. Underestimating the impact on employees and stakeholders and neglecting change management strategies can lead to resistance, decreased productivity, and project failure.

Avoiding these common mistakes requires a comprehensive approach, including thorough planning, ongoing risk assessment, and a commitment to staying informed about industry developments and best practices.

Conclusion

The landscape of industrial fintech services presents exciting opportunities for innovation and efficiency in the financial sector. However, success in this dynamic space requires a proactive approach to addressing common challenges.

Fintech companies must prioritize robust cybersecurity measures to safeguard sensitive data and maintain trust. Compliance with regulatory requirements is non-negotiable, and staying informed about evolving regulations is crucial for sustained operations.

Adequate customer education and user-friendly design are paramount to ensure seamless adoption and positive user experiences. Scalability planning, attention to data management practices, and interoperability with existing systems are vital considerations for long-term success.